Features

Industries

Who we serve

Resources

Sign in

Get Started - $500/month

No commitment. No implementation fee. Unlimited users. Cancel anytime

.jpg)

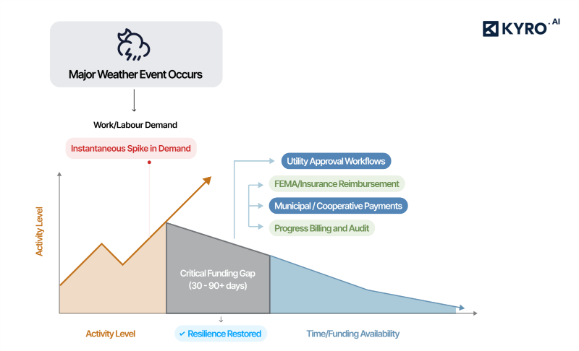

Storm restoration contractors operate in one of the most capital-intensive segments of the construction industry. After a major weather event, demand spikes instantly, while funding still moves through formal approval and reimbursement channels:

Meanwhile, costs are immediate:

Even well-run contractors can feel cash-constraints during extended storm seasons. Not because the work isn’t profitable, but because cash inflow and payments lag far behind execution.

And when cash flow tightens, the consequences show up quickly:

This is the operational problem invoice factoring is designed to address.

The Factor: The financial partner who purchases your invoices and provides immediate cash

The Customer: The Prime contractor or the Utility who settles the payment with the Factor.

The Client: The contractor or the Utility who gets the payment from the Factor.

Invoice factoring allows contractors to access cash tied up in completed, unpaid invoices. The process is straightforward:

For utility storm restoration contractors, this speed matters. While end-payers may take 60-120 days to process payments through account debtors, factoring ensures immediate cash flow to pay crews, maintain equipment, and mobilize for the next project.

Storm work pauses when invoices haven’t yet turned into usable cash. Faster access to funds helps contractors cover payroll, fuel, and lodging so crews can stay deployed, and restoration work continues without disruption.

When cash flow is predictable, project managers can plan work, schedule equipment, and coordinate vendors without constant financial contingency planning.

Paying crews and vendors on time builds trust in an industry where experienced storm labor is hard to retain, and supplier's availability is critical.

With working capital available, contractors aren’t forced to decline additional utility work simply because multiple invoices are pending. Invoice factoring doesn’t succeed on invoices alone. It succeeds on the quality of the data behind those invoices.

In utility storm restoration, payment delays often stem from:

Factoring partners face the same challenge. If invoices aren’t clear and defensible, advances slow down or shrink. So, how do you make invoices, Factoring Ready?

KYRO AI acts as a trusted source for accurate and validated work data. By standardizing how storm jobs flow from

Storm events → work orders → crew activities → timesheets → invoices

KYRO AI creates a clean, consistent record of all the work performed in a short span of time.

This structure helps ensure:

For contractors and sub-contractors, this means approved invoices are factoring-ready and faster for financing partners to verify, fund, and process.

Storm restoration doesn’t slow down when cash flow lags behind the work being done. When field execution, verified work data, and cash flow stay aligned, contractors gain what matters most in storm response: speed, predictability, and control.

By standardizing how work moves from the field to approved invoices, KYRO AI helps contractors get paid faster on approved invoices, keeping crews deployed, projects moving, and operations running without delays tied to payment cycles.

Factoring, also known as invoice factoring or accounts receivable factoring, is when a business sells its unpaid invoices to a third-party company for immediate cash. Rather than waiting 30-90 days for customer payments, businesses receive 70-90% of the invoice value within 24 hours.

This alternative financing method helps companies improve cash flow without taking on traditional debt. Factoring is particularly popular among small businesses, startups, and companies in industries like trucking, staffing, manufacturing, and wholesale distribution.

A factoring company (also called a factor or factoring agency) is a financial services provider that purchases your business's accounts receivable at a discount. These companies provide immediate working capital by buying your unpaid invoices.

Unlike banks or traditional lenders, factoring companies evaluate your customers' credit rather than your business credit score. The best factoring companies offer same-day funding, online portals for invoice submission, and flexible terms without long-term contracts.

Invoice factoring works in four simple steps:

The entire factoring process is typically completed within 30-90 days, depending on your customer's payment terms. This process converts slow-paying receivables into immediate working capital.

4. What is factoring accounts receivable?

Factoring accounts receivable is the practice of selling your outstanding invoices (accounts receivable) to a factoring company for quick cash. Accounts receivable factoring allows businesses to unlock capital tied up in unpaid customer invoices.

Instead of using accounts receivable as collateral for a loan, you're selling the actual invoices. This means factoring receivables doesn't create debt on your balance sheet. Common industries using AR factoring include transportation, staffing agencies, wholesalers, and government contractors.

Factoring companies charge 1% to 5% of the invoice value as their fee, with the average factoring rate ranging from 2% to 3% for creditworthy customers.

Factoring fee breakdown:

Factors affecting cost:

For example, on a $10,000 invoice with a 3% factoring fee, you'd receive approximately $8,000-$9,000 upfront and $700-$1,000 later (after the 3% fee is deducted).

Storm restoration contractors operate in one of the most capital-intensive segments of the construction industry. After a major weather event, demand spikes instantly, while funding still moves through formal approval and reimbursement channels:

Meanwhile, costs are immediate:

Even well-run contractors can feel cash-constraints during extended storm seasons. Not because the work isn’t profitable, but because cash inflow and payments lag far behind execution.

And when cash flow tightens, the consequences show up quickly:

This is the operational problem invoice factoring is designed to address.

The Factor: The financial partner who purchases your invoices and provides immediate cash

The Customer: The Prime contractor or the Utility who settles the payment with the Factor.

The Client: The contractor or the Utility who gets the payment from the Factor.

Invoice factoring allows contractors to access cash tied up in completed, unpaid invoices. The process is straightforward:

For utility storm restoration contractors, this speed matters. While end-payers may take 60-120 days to process payments through account debtors, factoring ensures immediate cash flow to pay crews, maintain equipment, and mobilize for the next project.

Storm work pauses when invoices haven’t yet turned into usable cash. Faster access to funds helps contractors cover payroll, fuel, and lodging so crews can stay deployed, and restoration work continues without disruption.

When cash flow is predictable, project managers can plan work, schedule equipment, and coordinate vendors without constant financial contingency planning.

Paying crews and vendors on time builds trust in an industry where experienced storm labor is hard to retain, and supplier's availability is critical.

With working capital available, contractors aren’t forced to decline additional utility work simply because multiple invoices are pending. Invoice factoring doesn’t succeed on invoices alone. It succeeds on the quality of the data behind those invoices.

In utility storm restoration, payment delays often stem from:

Factoring partners face the same challenge. If invoices aren’t clear and defensible, advances slow down or shrink. So, how do you make invoices, Factoring Ready?

KYRO AI acts as a trusted source for accurate and validated work data. By standardizing how storm jobs flow from

Storm events → work orders → crew activities → timesheets → invoices

KYRO AI creates a clean, consistent record of all the work performed in a short span of time.

This structure helps ensure:

For contractors and sub-contractors, this means approved invoices are factoring-ready and faster for financing partners to verify, fund, and process.

Storm restoration doesn’t slow down when cash flow lags behind the work being done. When field execution, verified work data, and cash flow stay aligned, contractors gain what matters most in storm response: speed, predictability, and control.

By standardizing how work moves from the field to approved invoices, KYRO AI helps contractors get paid faster on approved invoices, keeping crews deployed, projects moving, and operations running without delays tied to payment cycles.

Factoring, also known as invoice factoring or accounts receivable factoring, is when a business sells its unpaid invoices to a third-party company for immediate cash. Rather than waiting 30-90 days for customer payments, businesses receive 70-90% of the invoice value within 24 hours.

This alternative financing method helps companies improve cash flow without taking on traditional debt. Factoring is particularly popular among small businesses, startups, and companies in industries like trucking, staffing, manufacturing, and wholesale distribution.

A factoring company (also called a factor or factoring agency) is a financial services provider that purchases your business's accounts receivable at a discount. These companies provide immediate working capital by buying your unpaid invoices.

Unlike banks or traditional lenders, factoring companies evaluate your customers' credit rather than your business credit score. The best factoring companies offer same-day funding, online portals for invoice submission, and flexible terms without long-term contracts.

Invoice factoring works in four simple steps:

The entire factoring process is typically completed within 30-90 days, depending on your customer's payment terms. This process converts slow-paying receivables into immediate working capital.

4. What is factoring accounts receivable?

Factoring accounts receivable is the practice of selling your outstanding invoices (accounts receivable) to a factoring company for quick cash. Accounts receivable factoring allows businesses to unlock capital tied up in unpaid customer invoices.

Instead of using accounts receivable as collateral for a loan, you're selling the actual invoices. This means factoring receivables doesn't create debt on your balance sheet. Common industries using AR factoring include transportation, staffing agencies, wholesalers, and government contractors.

Factoring companies charge 1% to 5% of the invoice value as their fee, with the average factoring rate ranging from 2% to 3% for creditworthy customers.

Factoring fee breakdown:

Factors affecting cost:

For example, on a $10,000 invoice with a 3% factoring fee, you'd receive approximately $8,000-$9,000 upfront and $700-$1,000 later (after the 3% fee is deducted).

Rabiya Farheen is a content strategist and a writer who loves turning complex ideas into clear, meaningful stories, especially in the world of utility, tech, AI, and B2B SaaS. She works closely with growing teams to create content that doesn’t just check SEO boxes, but actually helps people understand what a product does and why it matters. With a knack for research and a curiosity that never quits, Rabiya dives deep into industry trends, customer pain points, and data to craft content that feels super helpful and informative. When she’s not writing, she’s probably reading, painting, and exploring her creative side— or you'll find her hustling around for social causes, especially those that empower girls and women.

.jpg)